- 销售与服务热线

- 400 886 9608

智能座舱快速普及,今年渗透率将破70%

近日,由盖世汽车研究院主办的“中国汽车新供应链配置数据产品发布会”在上海圆满召开。

盖世汽车研究院致力于成为汽车行业智库的领先者,通过以汽车供应链配置信息、整车产销量信息为核心底层数据资源,深度垂直聚焦智能汽车全产业链深度洞察,输出完善的汽车产业研究成果和完整的产业数据资源,进而支持行业用户进行商业决策。

此次中国汽车新供应链配置数据产品发布会上,盖世汽车面向市场隆重推出了乘用车智能驾驶配置数据库、乘用车智能座舱配置数据库、乘用车电气化配置数据库三套原创性数据库产品和配套市场分析月报。

近年来,智能电动汽车的蓬勃发展,推动以自动驾驶、智能座舱及三电技术为代表的新兴技术集群,开始逐步取代传统“三大件”,成为塑造车企核心竞争力、提升产品力的关键。尤其是智能座舱,得益于与先进车载显示、车载声学、人机交互以及座舱应用生态等的深度协同,正在开启新一轮增长周期,预计接下来几年整体市场规模有望超过千亿。

智能座舱加速渗透

作为一个复杂的集成化系统,智能座舱在业界其实并没有统一定义。这里盖世汽车研究院对于智能座舱的界定,特指同时搭载了8英寸以上中控屏、语音交互、车联网以及OTA功能的座舱系统。

其中中控屏和语音交互,主要是给用户提供出色的人机交互体验,提升操控便捷性及交互效率。而车联网以及OTA,则可以大幅拓宽整车的功能边界与应用场景维度,更好地满足终端用户的多元化诉求。

毕竟,如今智能电动汽车对于很多人而言,早已不再是简单的代步工具,同时还承担了用户对休闲娱乐、社交以及情感交互等的多重诉求,俨然人们除了居住和工作空间外的“第三生活空间”。

据相关分析数据显示,接近9成的国内用户在购车时会将智能座舱配置纳入考虑,同时超过6成的用户对座舱内的功能有付费意愿。具体细分功能来看,终端用户对车机芯片、语音识别、车联网、OTA、远程启动、高精地图以及手机映射等功能的偏好度相对较高,均超过了60%。

图片来源:盖世汽车

图片来源:盖世汽车

不过,更丰富的智能座舱功能,同时也意味着更复杂的软硬件系统集成,以及更高的量产搭载成本。

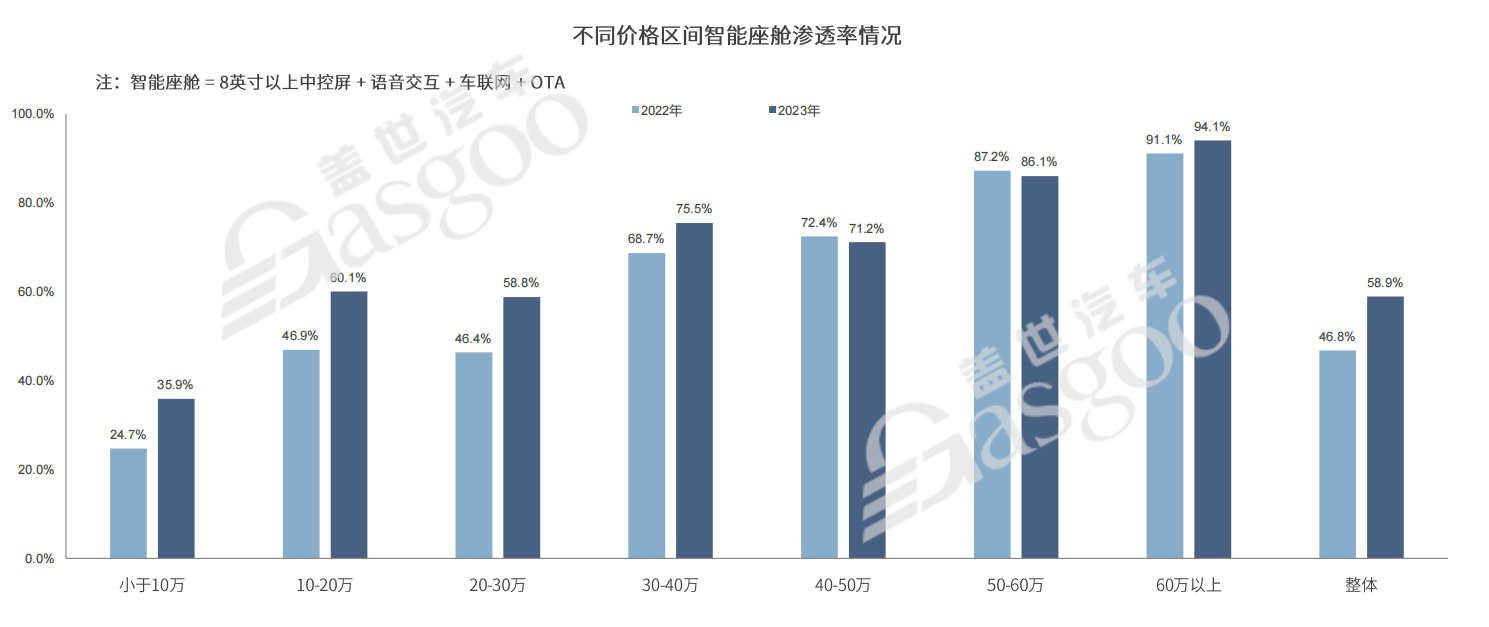

从终端市场搭载情况来看,目前智能座舱以30万元以上的市场整体配置率较高。其中30-50万元区间市场,2023年智能座舱渗透率高达70%,50万以上市场更是超过了80%。但这也不难理解,毕竟整车价格越高,对智能座舱系统的成本包容性也相对更强。

而30万元以下市场,以10-20万元区间智能座舱渗透率较高,约为60%,10万元以下市场渗透率最低,不足40%。

但如果从增量部分来看,去年智能座舱搭载率反而在30万元以下市场提升明显。特别是10-20万元市场,2023年智能座舱渗透率达60.1%,甚至高于20-30万元市场,相较于2022年提升近13个百分点。

这意味着,继中高端市场率先普及,如今智能座舱正呈现明显的配置下探趋势,在中低端市场配置率提升显著。

据盖世汽车研究院配置数据显示,当前国内智能座舱整体渗透率已接近60%。接下来随着整个产业链进一步成熟,驱动成本持续下探,预计智能座舱搭载率会继续提升,今年整体渗透率有望超过70%。

本土供应链崛起正当时

智能座舱作为汽车智能化的重要载体,其演进与创新深度依赖于车载显示、车载声学、先进人机交互以及高性能芯片等核心技术的深度融合与高效协同。

也正因如此,过去几年智能座舱的迅猛发展,除了带来终端用户驾乘体验革命性跃升,也有力驱动了相关核心产业链的成熟与繁荣,特别是自主供应链强势崛起。

图片来源:盖世汽车

图片来源:盖世汽车

以车载显示为例,由于整车功能复杂度持续提升,以及终端用户对车内空间数字化、个性化需求不断升级,使得座舱显示屏作为车内信息展示的核心载体与关键人机交互界面,在近年来呈现出明显的“大屏化”与“多屏化”趋势。

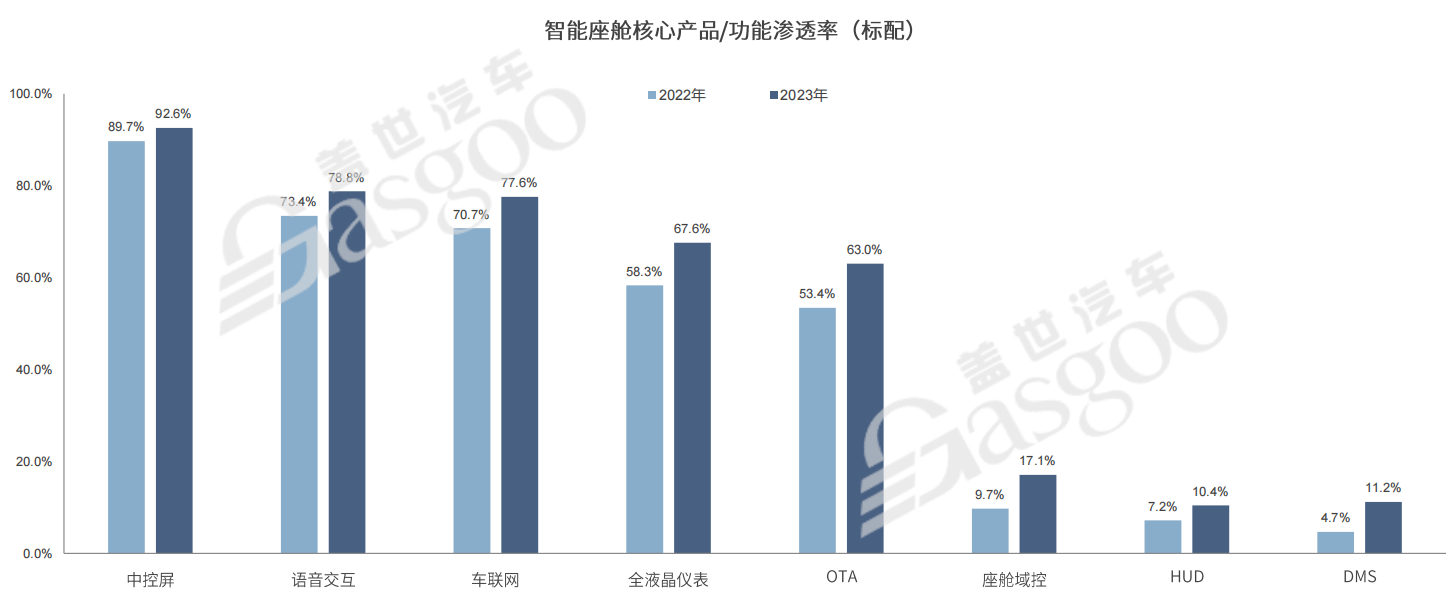

据盖世汽车研究院配置数据显示,2023年中控屏和液晶仪表在新车市场的渗透率分别达到了92.6%和67.6%,相较于2022年均有不同幅度的提升。

其中12-16英寸中控屏去年在座舱内的配置率高达42.1%,相较于2022年提升超10个百分点;8-12英寸中控屏搭载率虽有所下降,依然达到了42.2%;另外,更大尺寸的28英寸甚至40+英寸的中控屏,也开始在新车上搭载,比如银河E8(配置|询价),就搭载了一块45英寸的超大中控屏。对比之下,8英寸以下中控屏搭载率下滑明显,去年只有14.4%,同比下降近10个百分点。

而液晶仪表,也以10英寸以上配置率提升较为明显,2023年累计占比达53.9%,特别是10-12英寸液晶仪表,2023年渗透率达28%,相较于2022年提升6个百分点。10英寸以下搭载率则出现了一定幅度的下滑,降至了46.1%。

图片来源:盖世汽车

图片来源:盖世汽车

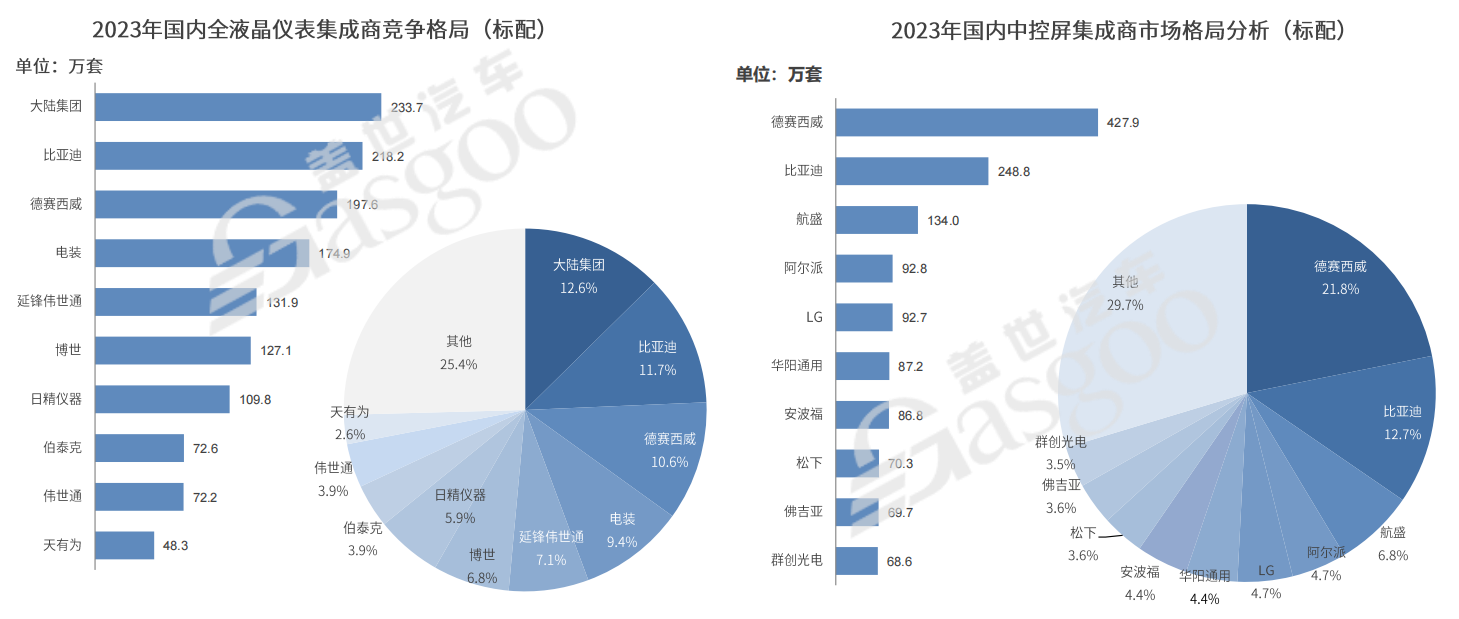

从核心供应商来看,中控屏以德赛西威和比亚迪占比较高,2023年装机量分别为427.9万套和248.8万套,对应市占率分别为21.8%和12.7%;液晶仪表则以大陆集团、比亚迪、德赛西威表现相对较好,2023年装机量分别为233.7万套、218.2 万套和197.6万套,CR3市场占比合计达34.9%。另外,京东方、TCL等跨界玩家也开始提供相关的配套。

除了大屏化趋势,在传统中控和仪表“双屏”基础上,近年来诸如HUD、副驾屏、后座娱乐屏、流媒体后视镜、透明A柱等创新显示技术,也开始在越来越多的新车上搭载,推动智能座舱朝着多屏化方向演进。

图片来源:盖世汽车

图片来源:盖世汽车

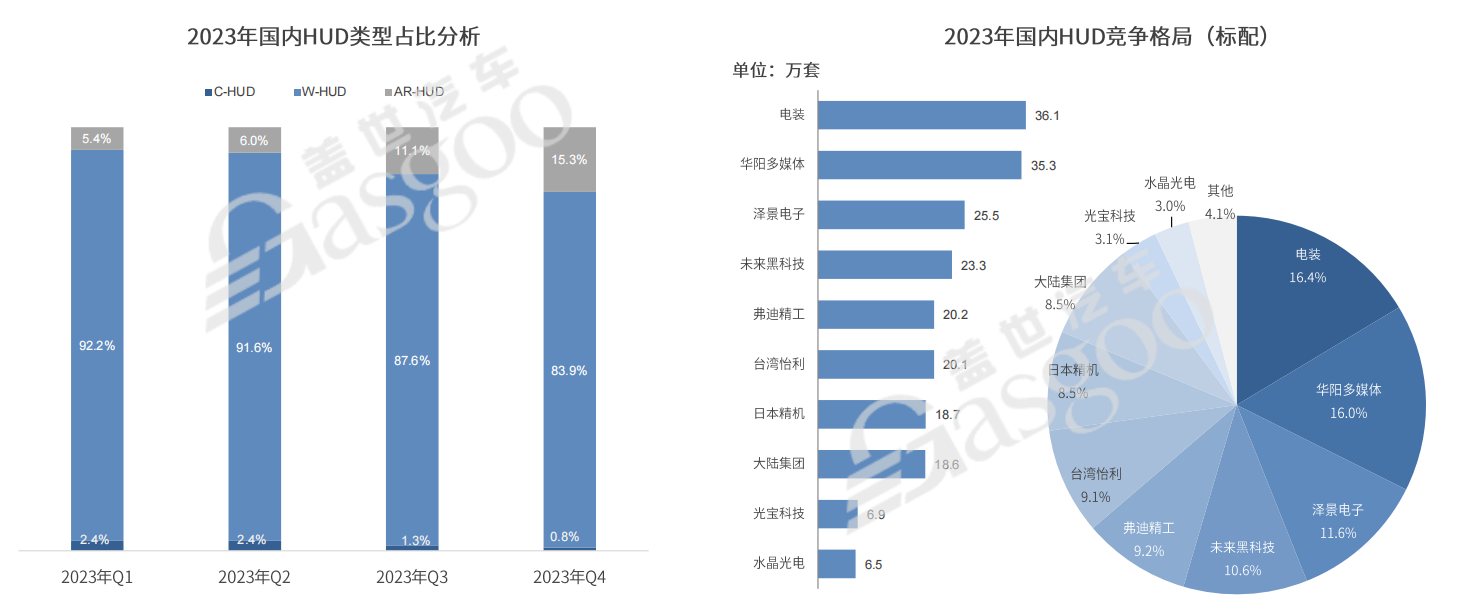

比如HUD,2023年渗透率已经达到了10.4%,W-HUD仍为主流配置方案,2023年占比接近9成。但更新一代的AR-HUD伴随着成本持续下降,也开始规模化上车,配置率从2023年Q1的5.4%提升到了Q4的15.3%。

从HUD市场格局来看,电装、华阳多媒体、泽景电子、未来黑科技、弗迪精工为主要配套供应商,2023年装机量分别达36.1万套、35.3万套、25.5万套、23.3万套和20.2万套,对应市场份额分别为16.4%、16%、11.6%、10.6%和9.2%,前五大供应商合计占据63.8%的市场份额。

图片来源:盖世汽车

图片来源:盖世汽车

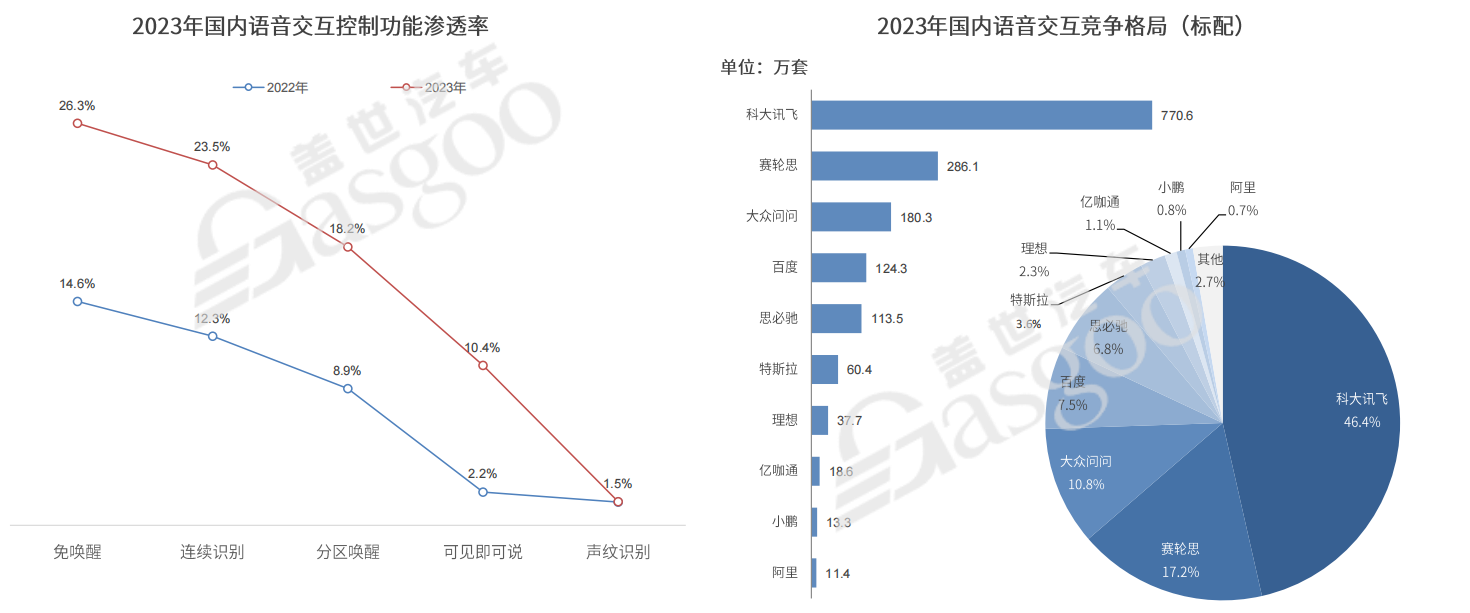

语音交互作为人与车最直接的沟通渠道,得益于AI技术快速发展,在车内的搭载率也呈现出稳定增长趋势,2023年渗透率达78.8%,相较于2022年提升5个百分点。其中免唤醒、连续识别、分区唤醒、可见即可说、声纹识别等语音交互相关功能,2023年搭载率均有明显提升。

具体到装机量,科大讯飞几乎占据半壁江山,2023年语音交互系统出货量达770.6万套,对应市场份额为46.4%。随后分别是赛轮思和大众问问,2023年装机量分别为286.1万套和180.3万套,对应市场份额分别为17.2%和10.8%,CR3市场占比合计超70%。

对于智能电动汽车,除了多元化座舱显示和智能化语音交互,赋予整车持续进化能力的OTA,同样成为了越来越多新车的标配。比如特斯拉和哈弗品牌,均已全系标配OTA,另外比亚迪也接近实现OTA标配,2023年渗透率为99.7%。

图片来源:盖世汽车

图片来源:盖世汽车

从OTA核心配套供应商来看,去年以比亚迪装机量最高,达238.8万套,对应市占率为17.9%。第三方供应商中间,则以艾拉比表现最好,去年累计装机量达159.1万套,市场份额为11.9%,其次是哈曼,2023年装机量为127万套,对应市占率为9.5%。

另外,得益于智能驾驶的快速发展,预计未来很长一段时间智能电动汽车将处于人机共驾阶段,由此驱动DMS作为一项核心配置,也开始广泛普及。比如理想汽车、极氪、问界等品牌,2023年DMS渗透率均已超过95%。不过目前DMS主要用于驾驶员监测,未来有望与更多的ADAS功能融合,为驾乘者提供全场景的服务应用。

整体来看,在本轮座舱智能化升级进程中,本土厂商作为重要的变革推手,不仅有力推动了座舱技术的革新迭代,还有效激发了自主新供应链从无到有、从弱到强的蜕变过程,为中国汽车产业在智能化时代抢占全球竞争制高点奠定了坚实基础。

下一个赛点:手车融合与大模型上车

如果按照中国汽车工程学会此前发布的《汽车智能座舱分级与综合评价白皮书》里的分级标准,现阶段智能座舱整体已经处于L2部分认知阶段,即具备舱内部分场景主动感知驾乘人员的能力,并可以主动执行部分任务,包括跨部分舱内外场景应用。

图片来源:盖世汽车

图片来源:盖世汽车

在此基础上,下一步智能座舱还将如何进行功能的迭代升级?

目前来看,基于手车互联的跨场景融合、AI大模型上车以及多操作系统的融合统一,正成为赛道新的角力点。

比如在跨场景互联方面,以华为鸿蒙、魅族Flyme Auto等为代表的新一代操作系统,凭借强大的系统兼容性与扩展能力,已经成功引入并优化了大量移动端应用至车载环境,包括传统车载功能的智能化升级,如导航、娱乐、通讯等,甚至还催生了诸多创新服务,如远程控制、车家互联、个性化推荐等,极大地丰富了座舱应用矩阵。

事实上,汽车和手机的跨场景互联并非一项新应用,不过早期两者之间的跨终端互联主要是借助苹果Carplay、百度CarLife等手机映射系统来实现,不仅功能单一,而且只能通过中控屏单向控制手机。

图片来源:盖世汽车

图片来源:盖世汽车

而当前新一代手车互联方案,除了能够兼容更多的生态应用,还可以实现手机与车机的双向控制,并支持跨终端算力共。比如华为HiCar,就支持车机、手机的硬件调用和算力共享等功能,另外还有魅族Flyme Link以及小米CarWith,均支持手机端与车机端算力共享,以及手机和车机之间的双向控制。

据盖世汽车研究院配置数据显示,2023年手机互联映射功能在新车市场的渗透率约为56.4%,其中百度CarLife和苹果Carplay依然是主流方案,去年渗透率分别为33.4%和30.7%,同时华为HiCar搭载率也在持续提升,去年配置率达8.5%,较2022年提升3个百分点。

另外随着汽车网联化程度越来越高,通过手机APP远程控制汽车也开始成为主流,去年APP远程控制功能渗透率突破了60%,其中车辆监控、远程控制、服务预约等功能渗透率均超过50%。

分品牌来看,海外豪华品牌整体对手机映射功能的依赖度较高,而自主品牌由于车机系统的生态相对完善,对映射功能依赖较小,反而对手机APP远程控制功能的依赖相对较高,去年整体渗透率超过了75%。

按照目前的趋势,未来手机除了作为数据采集的入口,还可以通过与汽车实现基于操作系统的跨终端互联,以及共享算力、传感器等,实现更多的交互应用,打造真正的“人-车-生活”生态闭环,实现多场景无缝衔接。

还有大模型上车,也是智能座舱下一阶段角逐的重点。

过去几年里,尽管座舱智能化进程已经取得显著突破,尤其在语音交互方面,通过与AI技术的深度融合,众多车载语音助手已展现出初步的拟人化特征。不可否认,当前车载语音系统底层仍然是没有完全成熟的任务型对话系统,无法真正实现个性化和情感化的交互。

图片来源:梅赛德斯-奔驰

图片来源:梅赛德斯-奔驰

2023年,大模型爆火让业界看到了智能座舱新的升级方向,并纷纷开展布局。比如百度和吉利共同打造的极越01(配置|询价),已经实现了百度“文心一言”语音大模型上车,将极越01的人机交互体验提升到了一个新高度。科大讯飞的星火认知大模型也已首搭奇瑞星纪元ES(配置|询价),目标打造更有情感的极致智能座舱体验。另外,理想、蔚来、小鹏、吉利、比亚迪、奔驰等车企,也均在争相推动大模型上车。按照目前趋势,今年有望成为座舱大模型批量上车元年。

值得关注的是,大模型上车除了可以助力实现更加个性化和智能化的驾乘体验,让汽车真正具备逻辑能力、决策能力和生成能力,实现从功能车向智能车的进化,还有望通过个性化的车主服务,推动智能座舱商业模式变革。

展望未来,智能电动汽车发展方兴未艾,属于智能座舱的变革,也远未到终局。

Intelligent cabins are rapidly becoming popular, with penetration rates expected to exceed 70% this year

Recently, the "China Automotive New Supply Chain Configuration Data Product Launch Conference" hosted by GAC Automotive Research Institute was successfully held in Shanghai.

GAC Automotive Research Institute is committed to becoming a leader in the automotive industry think tank. By focusing on automotive supply chain configuration information and vehicle production and sales information as the core underlying data resources, GAC Automotive Research Institute provides in-depth insights into the entire intelligent automotive industry chain, outputs comprehensive automotive industry research results and complete industry data resources, and supports industry users in making business decisions.

At the launch of the new supply chain configuration data product launch event for Chinese automobiles, GAC Motor launched three sets of original database products and supporting market analysis monthly reports, including the intelligent driving configuration database for passenger cars, the intelligent cockpit configuration database for passenger cars, and the electrification configuration database for passenger cars.

In recent years, the booming development of intelligent electric vehicles has driven emerging technology clusters represented by autonomous driving, intelligent cockpit, and three electric technologies to gradually replace traditional "three major components", becoming the key to shaping the core competitiveness of automotive enterprises and enhancing product strength. Especially the intelligent cockpit, benefiting from deep collaboration with advanced in car displays, in car acoustics, human-computer interaction, and cockpit application ecology, is entering a new growth cycle, and it is expected that the overall market size will exceed 100 billion in the coming years.

Intelligent cockpit acceleration penetration

As a complex integrated system, there is actually no unified definition of intelligent cockpit in the industry. The definition of intelligent cockpit by GAC Automotive Research Institute specifically refers to a cockpit system that is equipped with a central control screen of 8 inches or more, voice interaction, vehicle networking, and OTA functions.

The central control screen and voice interaction mainly provide users with an excellent human-computer interaction experience, improving control convenience and interaction efficiency. The Internet of Vehicles and OTA can significantly expand the functional boundaries and application scenario dimensions of the entire vehicle, better meeting the diversified demands of end users.

After all, smart electric vehicles are no longer a simple means of transportation for many people nowadays. They also bear the multiple demands of users for leisure, entertainment, social interaction, and emotional interaction, becoming the "third living space" for people besides living and working spaces.

According to relevant analysis data, nearly 90% of domestic users consider intelligent cockpit configuration when purchasing a car, and over 60% of users have a willingness to pay for the functions inside the cockpit. In terms of specific segmentation functions, end users have a relatively high preference for features such as car infotainment chips, voice recognition, car networking, OTA, remote start, high-precision maps, and mobile phone mapping, all exceeding 60%.

Image source: GAC Motor

However, richer intelligent cockpit functions also mean more complex software and hardware system integration, as well as higher production carrying costs.

From the perspective of terminal market deployment, the overall configuration rate of intelligent cabins in the market is relatively high with a price of over 300000 yuan. Among them, the market in the range of 300000 to 500000 yuan has a penetration rate of up to 70% for intelligent cabins in 2023, and the market above 500000 yuan has exceeded 80%. But this is not difficult to understand, after all, the higher the price of the entire vehicle, the stronger the cost tolerance for the intelligent cockpit system.

In the market below 300000 yuan, the penetration rate of intelligent cabins in the 100000 to 200000 yuan range is relatively high, about 60%, while the penetration rate in the market below 100000 yuan is the lowest, less than 40%.

But if we look at the incremental part, the market saw a significant increase in the intelligent cockpit occupancy rate last year, which was below 300000 yuan. Especially in the 100000 to 200000 yuan market, the penetration rate of intelligent cabins reached 60.1% in 2023, even higher than the 200000 to 300000 yuan market, an increase of nearly 13 percentage points compared to 2022.

This means that, following the lead in popularization in the mid to high end market, intelligent cabins are now showing a clear downward trend in configuration, with a significant increase in configuration rate in the mid to low end market.

According to configuration data from GAC Automotive Research Institute, the overall penetration rate of intelligent cabins in China has reached nearly 60%. As the entire industry chain further matures and driving costs continue to decline, it is expected that the intelligent cockpit occupancy rate will continue to increase, and the overall penetration rate is expected to exceed 70% this year.

The rise of local supply chains is at the right time

As an important carrier of automotive intelligence, the evolution and innovation of intelligent cabins rely heavily on the deep integration and efficient collaboration of core technologies such as in car displays, in car acoustics, advanced human-computer interaction, and high-performance chips.

As a result, the rapid development of intelligent cabins in the past few years has not only brought about a revolutionary leap in the driving experience of end users, but also effectively driven the maturity and prosperity of related core industrial chains, especially the strong rise of independent supply chains.

Image source: GAC Motor

Taking in car displays as an example, due to the continuous increase in the complexity of vehicle functions and the upgrading of end users' digital and personalized needs for interior space, the cockpit display screen, as the core carrier of interior information display and key human-computer interaction interface, has shown a clear trend of "large screen" and "multi screen" in recent years.

According to configuration data from the GAC Automotive Research Institute, the penetration rates of the central control screen and LCD instrument panel in the new car market reached 92.6% and 67.6% respectively in 2023, with varying degrees of improvement compared to the average annual growth rate in 2022.

The configuration rate of the 12-16 inch central control screen in the cabin reached 42.1% last year, an increase of over 10 percentage points compared to 2022; Although the loading rate of the 8-12 inch central control screen has decreased, it still reaches 42.2%; In addition, larger 28 inch or even 40+inch central control screens are also being installed in new cars, such as the Galaxy E8 (configuration | inquiry), which is equipped with a large 45 inch central control screen. In contrast, the occupancy rate of central control screens below 8 inches has significantly declined, with only 14.4% last year, a decrease of nearly 10 percentage points year-on-year.

The LCD instrument panel has also seen a significant increase in configuration rates above 10 inches, with a cumulative proportion of 53.9% in 2023. Especially for the 10-12 inch LCD instrument panel, the penetration rate reached 28% in 2023, an increase of 6 percentage points compared to 2022. The loading rate of less than 10 inches has decreased to a certain extent, dropping to 46.1%.

Image source: GAC Motor

From the perspective of core suppliers, Desai Xiwei and BYD have a relatively high proportion of central control screens, with installed capacity of 4.279 million units and 2.488 million units in 2023, corresponding to market share of 21.8% and 12.7%, respectively; The performance of LCD instruments is relatively good among Continental Group, BYD, and Desai Xiwei, with installed capacity of 2.337 million sets, 2.182 million sets, and 1.976 million sets in 2023, respectively. The total market share of CR3 is 34.9%. In addition, cross-border players such as BOE and TCL have also begun to provide relevant supporting facilities.

In addition to the trend of large screens, in recent years, innovative display technologies such as HUD, passenger screen, rear entertainment screen, streaming rearview mirror, transparent A-pillar, etc. have also begun to be installed on more and more new cars, promoting the evolution of intelligent cabins towards multi screen design, based on the traditional dual screen control and instrument panel.

Image source: GAC Motor

For example, HUD has achieved a penetration rate of 10.4% in 2023, while W-HUD remains the mainstream configuration solution, accounting for nearly 90% in 2023. But with the continuous decrease in costs, the updated generation of AR-HUD has also begun to be scaled up, with a configuration rate increasing from 5.4% in Q1 2023 to 15.3% in Q4.

From the perspective of the HUD market pattern, Dianzhuang, Huayang Multimedia, Zejing Electronics, Future Black Technology, and Fodi Precision Industry are the main supporting suppliers. In 2023, their installed capacity reached 361000 sets, 353000 sets, 255000 sets, 233000 sets, and 202000 sets, respectively, with corresponding market shares of 16.4%, 16%, 11.6%, 10.6%, and 9.2%. The top five suppliers together occupy 63.8% of the market share.

Image source: GAC Motor

As the most direct communication channel between people and vehicles, voice interaction has benefited from the rapid development of AI technology, and the loading rate in vehicles has also shown a stable growth trend. In 2023, the penetration rate reached 78.8%, an increase of 5 percentage points compared to 2022. Among them, voice interaction related functions such as wake-up free, continuous recognition, zone wake-up, visible and talkable, voiceprint recognition, etc. have significantly increased their occupancy rate in 2023.

Specifically, in terms of installed capacity, iFlytek almost occupies half of the market share. In 2023, the shipment volume of voice interaction systems reached 7.706 million sets, corresponding to a market share of 46.4%. Subsequently, Sailun Si and Volkswagen were asked. The installed capacity in 2023 was 2.861 million units and 1.803 million units, respectively, with corresponding market shares of 17.2% and 10.8%. The total market share of CR3 exceeded 70%.

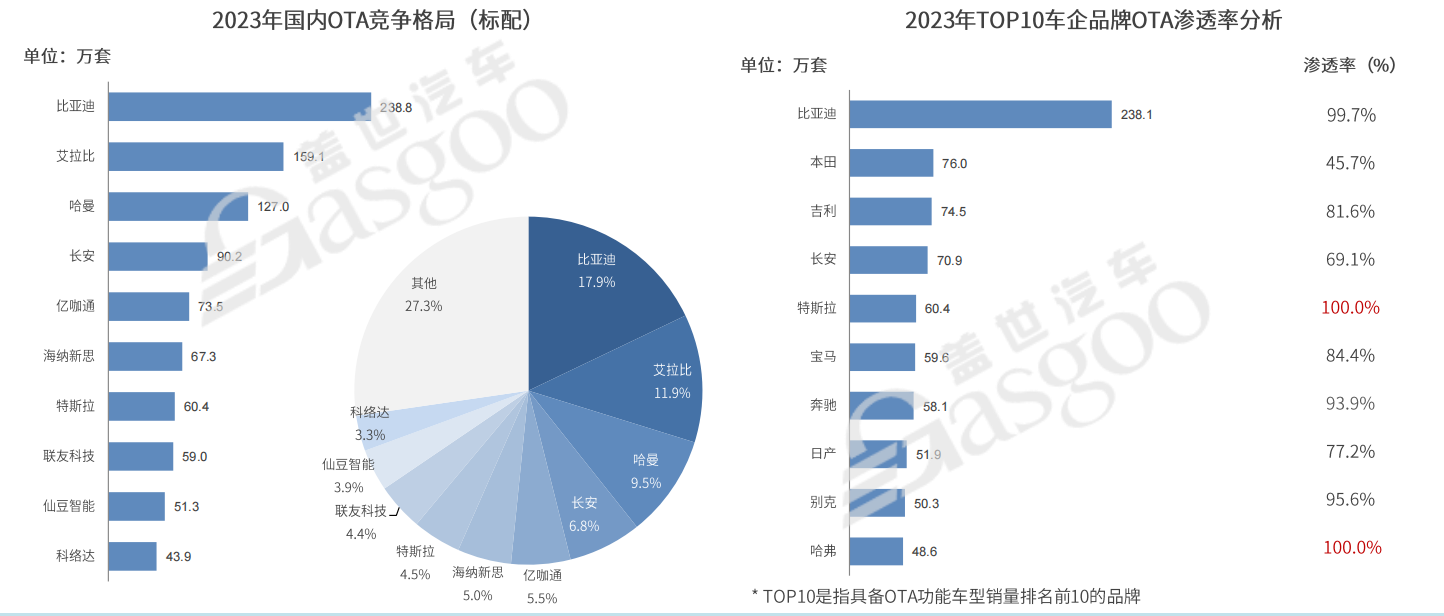

For intelligent electric vehicles, in addition to diversified cockpit displays and intelligent voice interaction, OTA, which endows the entire vehicle with continuous evolution ability, has also become a standard feature for more and more new cars. For example, Tesla and Haval brands are already equipped with OTA as standard across their entire lineup, and BYD is also close to achieving OTA as standard, with a penetration rate of 99.7% in 2023.

Image source: GAC Motor

From the perspective of OTA core supporting suppliers, BYD had the highest installed capacity last year, reaching 2.388 million units, corresponding to a market share of 17.9%. Among third-party suppliers, Elraby performed the best, with a cumulative installed capacity of 1.591 million units last year and a market share of 11.9%, followed by Harman. In 2023, the installed capacity was 1.27 million units, corresponding to a market share of 9.5%.

In addition, thanks to the rapid development of intelligent driving, it is expected that intelligent electric vehicles will be in the stage of human-machine co driving for a long time in the future. Therefore, driving DMS as a core configuration has also begun to be widely popularized. For example, brands such as Ideal Automobile, Jike, and Wenjie have achieved DMS penetration rates of over 95% in 2023. However, currently DMS is mainly used for driver monitoring and is expected to integrate with more ADAS functions in the future, providing drivers and passengers with full scenario service applications.

Overall, in this round of cockpit intelligent upgrading process, local manufacturers, as an important driving force for change, not only effectively promoted the innovation and iteration of cockpit technology, but also effectively stimulated the transformation process of independent new supply chains from scratch and from weak to strong, laying a solid foundation for China's automotive industry to seize the global competitive high ground in the era of intelligence.

Next race point: Handcart fusion and large model boarding

If we follow the classification standards in the White Paper on Classification and Comprehensive Evaluation of Intelligent Cabins for Automobiles previously released by the Chinese Society of Automotive Engineering, the intelligent cockpit as a whole is currently in the L2 cognitive stage, which means it has the ability to actively perceive the driver and passengers in certain scenarios inside the cabin, and can actively perform certain tasks, including applications across different indoor and outdoor scenarios.

Image source: GAC Motor

On this basis, how will the next step of the intelligent cockpit be to iterate and upgrade its functions?

At present, cross scene fusion based on handcart interconnection, AI large model loading, and the integration and unification of multiple operating systems are becoming new competition points on the track.

For example, in terms of cross scenario interconnection, the new generation operating systems represented by Huawei HarmonyOS, Meizu Flyme Auto, etc., with strong system compatibility and scalability, have successfully introduced and optimized a large number of mobile applications to the in car environment, including the intelligent upgrade of traditional in car functions such as navigation, entertainment, communication, and even spawned many innovative services, such as remote control, car home interconnection, personalized recommendation, etc., greatly enriching the cockpit application matrix.

In fact, the cross scenario interconnection between cars and mobile phones is not a new application. However, in the early days, the cross terminal interconnection between the two was mainly achieved through mobile mapping systems such as Apple Carplay and Baidu CarLife. Not only was the function single, but the phone could only be controlled unidirectionally through the central control screen.

Image source: GAC Motor

The current new generation of handcart interconnection solutions, in addition to being compatible with more ecological applications, can also achieve bidirectional control between mobile phones and car phones, and support cross terminal computing power sharing. For example, Huawei HiCar supports hardware calls and computing power sharing for car and mobile devices. In addition, Meizu Flyme Link and Xiaomi CarWith both support computing power sharing between mobile and car devices, as well as bidirectional control between mobile and car devices.

According to configuration data from GAC Automotive Research Institute, the penetration rate of mobile connectivity mapping function in the new car market is about 56.4% in 2023. Baidu CarLife and Apple Carplay are still mainstream solutions, with penetration rates of 33.4% and 30.7% last year, respectively. At the same time, Huawei HiCar's occupancy rate is also continuously increasing, reaching 8.5% last year, an increase of 3 percentage points from 2022.

In addition, with the increasing degree of car networking, remote control of cars through mobile apps has also become mainstream. Last year, the penetration rate of APP remote control functions exceeded 60%, with vehicle monitoring, remote control, service reservation and other functions all exceeding 50%.

From a brand perspective, overseas luxury brands generally have a high dependence on mobile phone mapping functions, while domestic brands, due to the relatively complete ecosystem of car infotainment systems, have a relatively low dependence on mapping functions. On the contrary, they have a relatively high dependence on remote control functions of mobile apps, with an overall penetration rate exceeding 75% last year.

According to the current trend, in the future, mobile phones can not only serve as an entry point for data collection, but also achieve cross terminal interconnection based on operating systems with cars, as well as share computing power, sensors, etc., to achieve more interactive applications, create a true "person vehicle life" ecological loop, and achieve seamless connection of multiple scenarios.

There is also a large model on board, which is also the focus of the next stage of competition in the intelligent cockpit.

In the past few years, although significant breakthroughs have been made in the process of cabin intelligence, especially in the field of voice interaction, many in car voice assistants have shown preliminary anthropomorphic features through deep integration with AI technology. It is undeniable that the current in car voice system still lacks a fully mature task-based dialogue system, which cannot truly achieve personalized and emotional interaction.

Image source: Mercedes Benz

In 2023, the explosion of large models has shown the industry a new direction for upgrading intelligent cabins, and they have launched various layouts. For example, the Jiyue 01 (configuration | inquiry) jointly created by Baidu and Geely has realized the launch of Baidu's "ERNIE Bot" voice model, which has raised the human-computer interaction experience of Jiyue 01 to a new height. IFLYTEK's Spark Cognitive Model has also made its debut with the Chery Star Era ES (configuration | inquiry), aiming to create a more emotional and ultimate intelligent cockpit experience. In addition, car companies such as Ideal, NIO, Xiaopeng, Geely, BYD, Mercedes Benz, etc. are also competing to promote the launch of large models. According to the current trend, this year is expected to become the first year for mass production of large cabin models.

It is worth noting that in addition to helping to achieve a more personalized and intelligent driving experience, large models can truly equip cars with logical, decision-making, and generative abilities, enabling the evolution from functional vehicles to intelligent vehicles. It is also hoped that personalized owner services can promote the transformation of the intelligent cockpit business model.

Looking ahead to the future, the development of intelligent electric vehicles is still thriving, and it belongs to the transformation of intelligent cabins, which is far from the end.